Cash Flow Flywheel Tracker

Stop guessing where your money is going. Start tracking the assets, income streams, expenses, and accounts that move you closer to your Freedom Number.

Track the Whole Picture

See assets, liabilities, income streams, accounts, and expenses in one organized workbook.

Find the Leaks

Identify where money is producing, where it is sitting still, and where it may be slowing your flywheel.

Build With Clarity

Use the tracker weekly, monthly, or quarterly to review your financial progress like a system.

Most People Do Not Have a Money Problem. They Have a Tracking Problem.

They make money. They pay bills. They invest a little. They check accounts randomly. Then they wonder why their wealth still feels scattered.

The problem is simple: you cannot build a wealth machine if you cannot see where your money is flowing.

The Cash Flow Flywheel Tracker helps you organize your financial life like a system instead of a pile of disconnected accounts.

This is for the builder who wants every dollar to do more than one job.

A dollar can reduce risk. A dollar can buy an asset. A dollar can create cash flow. A dollar can lower debt. A dollar can move you closer to your Freedom Number. But only if you know where it is going.

What’s Inside the Tracker

The Real Cost Is Not the Price of the Tracker

The real cost is continuing to make money decisions without a clear view of your own numbers.

That is how people stay busy but not better. They work hard, earn, spend, invest randomly, forget to review, and lose track of what is producing versus what is draining.

This tracker gives you a simple place to slow down, organize the numbers, and see whether your cash flow flywheel is actually spinning faster.

Use It to Answer Better Money Questions

- What assets are actually producing income?

- What accounts are helping me move toward financial freedom?

- Where is my money stuck?

- What income streams are growing?

- What expenses are slowing the flywheel?

- Am I building a system or just collecting accounts?

Who This Is For

This tracker is for people building a second income stream, dividend investors, real estate investors, side-income builders, small business owners, people tracking their Freedom Number, and anyone who wants to turn scattered financial information into a simple review system.

Who This Is Not For

This is not for someone looking for a get-rich-quick promise, a magic stock pick, or financial advice without doing the tracking work.

This is for builders. People who understand that money gets stronger when it gets organized.

Track the Money. Find the Leaks. Build the Flywheel.

Download the Cash Flow Flywheel Tracker and begin reviewing your money like a system.

Get the Tracker on GumroadDisclaimer: This product is for educational and organizational purposes only. It is not financial, investment, tax, legal, or accounting advice. Always consult a qualified professional before making financial decisions.

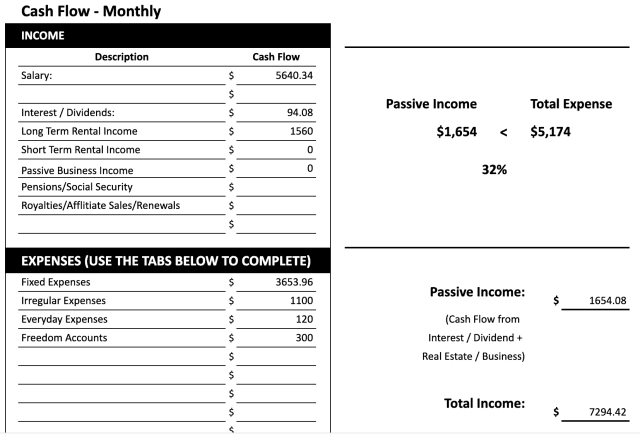

Incomes Versus Expenses